Today we will be answering the question, “Is a HELOC a mortgage?” Let’s begin by exploring what a HELOC is. A HELOC stands for Home Equity Line of Credit and is a type of loan. However, instead of getting all the money at once, you can instead borrow as you need. It works like a credit card. You have a limit and only pay interest on what you borrow.

How Does a HELOC Work?

- Equity Check: First, you need equity in your home. Equity is the difference between your home’s value and what you owe on it.

- Get Approved: You apply, and if approved, you get a line of credit.

- Draw Period: You can borrow during the draw period, which is usually 10 years.

- Repayment Period: After the draw period, you enter the repayment period. This can last 20 years. During this time you pay back what you borrowed, plus interest.

Is a HELOC a Mortgage?

Yes and no. Let’s break it down.

How They Are Similar:

- Secured by Your Home: Both HELOCs and mortgages are secured by your home. If you don’t pay, you could lose your home.

- Interest Payments: You pay interest on both.

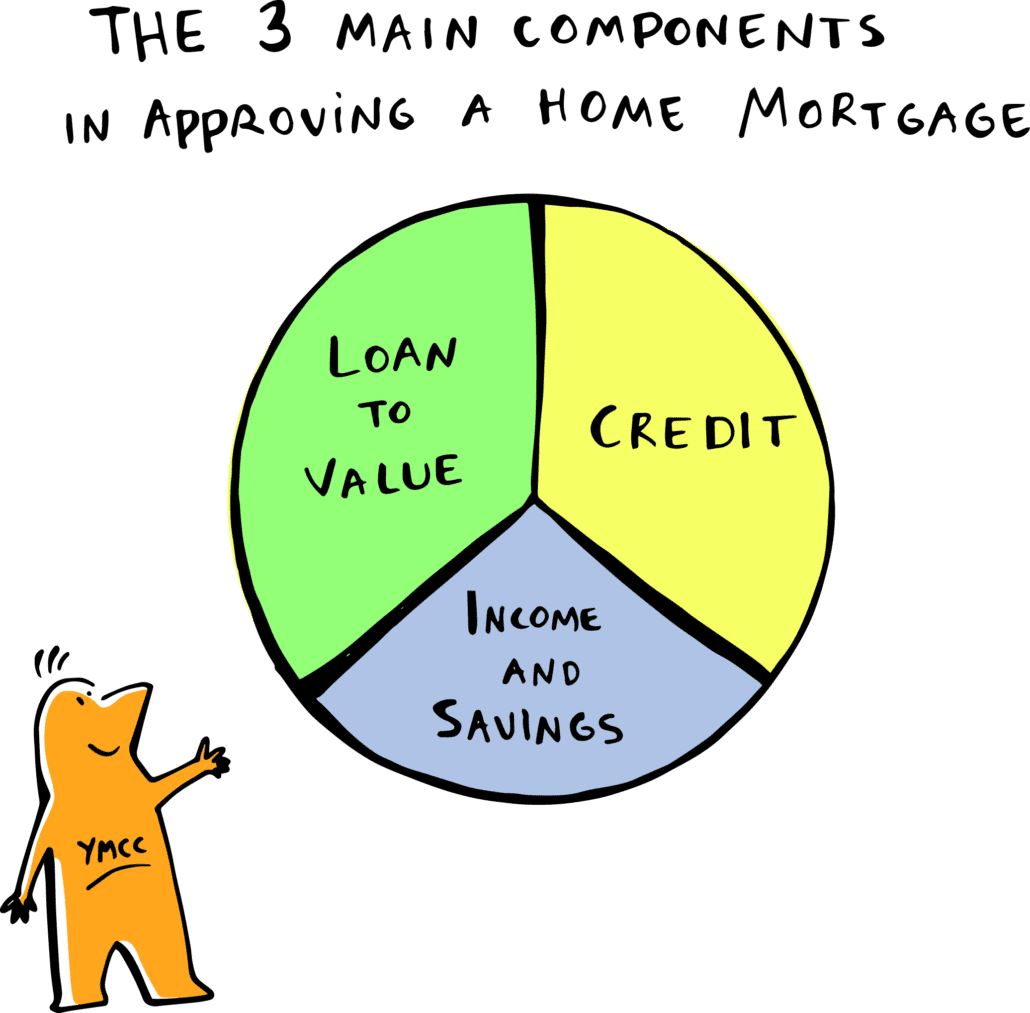

- Approval Process: Both need approval. Lenders will look at your credit, income, and home value.

How They Are Different:

- Upfront Money: A mortgage gives you a lump sum. A HELOC on the other hand lets you borrow as needed.

- Use of Funds: Mortgages usually buy a home. HELOCs however can be used for anything, such as home repairs, education, or paying off debt.

- Repayment Terms: Mortgage payments are fixed, whereas HELOC payments can vary based on how much you borrow.

Pros and Cons of a HELOC

Pros:

- Flexibility: Borrow what you need when you need it.

- Lower Interest Rates: Usually lower than credit cards.

- Tax Benefits: Interest may be tax-deductible.

Cons:

- Variable Rates: Interest rates can go up.

- Risk of Losing Home: If you can’t pay, you might lose your home.

- Temptation to Overspend: Easy access to funds can lead to overspending.

When to Use a HELOC

- Home Improvements: Boost your home’s value.

- Debt Consolidation: Pay off high-interest debt.

- Emergency Funds: Have a backup for unexpected costs.

Conclusion

A HELOC is a useful tool. It’s similar to a mortgage in some ways but different in others. It gives you flexibility and access to funds when you need them. Keep in mind, it’s still a loan secured by your home. By using it wisely you can enjoy the benefits it offers!

Contact Us Today!

Do you need help navigating your financial future? Contact us today!