Today we are going to discuss why you should stop using snowball & avalanche (do this instead). There’s a Better Way to Get Out of Debt Most people try to get out of debt the same way. They use the snowball or the avalanche, and at first, it feels like the right move. However, life happens. Payments feel heavy, stress builds, and soon it gets hard to keep going. So, instead of getting ahead, people get stuck. But there is a better way, and it starts with one simple idea: pay the bank less.

Why Snowball & Avalanche Feel So Hard

The snowball method says to start with the smallest debt first, while the avalanche method says to start with the highest interest rate. Both sound smart, and yes, they can work. But here’s the problem: they don’t lower your payments, they don’t reduce your stress, and most importantly, they don’t fix the real issue. So even if you follow the plan, you still feel tight every month. Because of that, many people quit before they ever see real progress.

The Real Problem Is the Cost of Your Debt

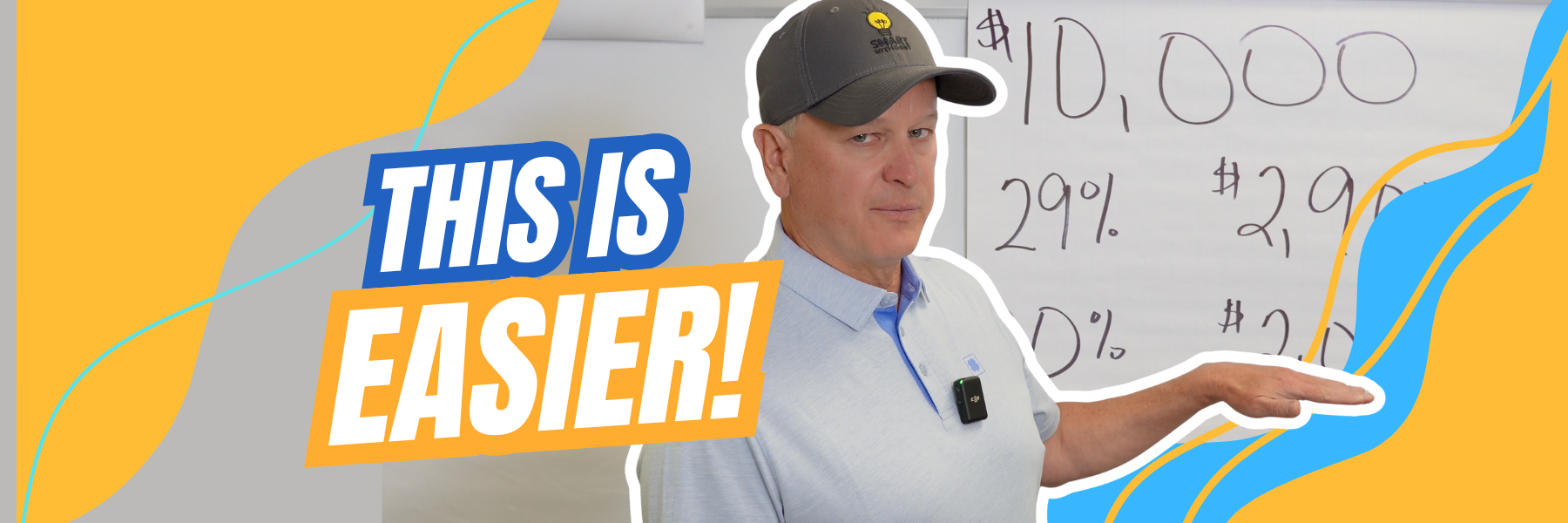

Before you try to pay off debt faster, you need to ask one simple question: what is my debt costing me? Not all debt is the same. In fact, two people can have the same $10,000 but pay very different amounts for it. For example, one person with a store credit card at 29% might pay about $2,900 per year in interest, while another with a regular credit card at 20% might pay about $2,000. Meanwhile, someone with a personal loan at 12% might pay $1,200, and someone with a home equity loan at 8% might pay $800. Finally, a person using a 0% card with a fee might only pay about $400. Same debt, very different cost.

Why Lowering Your Rate Changes Everything

Now, think about what that means. One person is paying over seven times more than another, even though the balance is the same. Because of that, one person struggles to make progress, while the other builds momentum quickly. So, it’s not just about how much debt you have. Instead, it’s about how much that debt is costing you every single month.

A Simple Example That Shows the Difference

Let’s take it one step further. Imagine you are paying $410 per month. With high-interest debt, you might be in debt for over three years and pay about $15,200 total. However, if you move that same debt into a lower-cost option, you could be done in about two years and pay around $11,552. And if you lower the cost even more, you might finish in just over two years and pay closer to $10,950. So not only do you get out of debt faster, but you also keep thousands of dollars and gain months of your life back.

The Better Strategy (What to Do Instead)

Because of this, the better strategy is simple. First, lower the cost of your debt. You can do that by looking at options like lower-rate personal loans, fixed-rate home equity loans, 0% balance transfer cards, or even credit union programs. Once you lower your rate, everything gets easier. Next, keep your payment the same. That way, more of your money goes toward the balance and less goes to interest. As a result, you move faster without working harder. Then, let momentum work for you. As your balance drops faster, your stress goes down, and your confidence starts to grow.

Two Ways to Win From Here

At this point, you actually have two strong options. First, you can keep your payment high and get out of debt faster, which means you finish sooner and pay less overall. Or second, you can lower your payment a bit and enjoy life now, whether that means going out more, helping family, or simply having more breathing room. Either way, you are still moving forward with a better plan.

Why This Works Better Than Snowball

The reason this works is simple. Snowball and avalanche focus on the order of your debts, while this strategy focuses on the cost. And cost is what really matters. You cannot out-earn high interest, and you cannot out-save bad debt. However, you can win when you pay less for your money.

Final Thought: Pay the Bank Less

At the end of the day, you don’t need another job, a strict budget, or to stop enjoying life. Instead, you need better debt. When you lower the cost, you create breathing room, build momentum, and get your life back sooner. So before you try to work harder, take a step back, look at your rates, and run the numbers. Because once you do, you will see a better path forward.